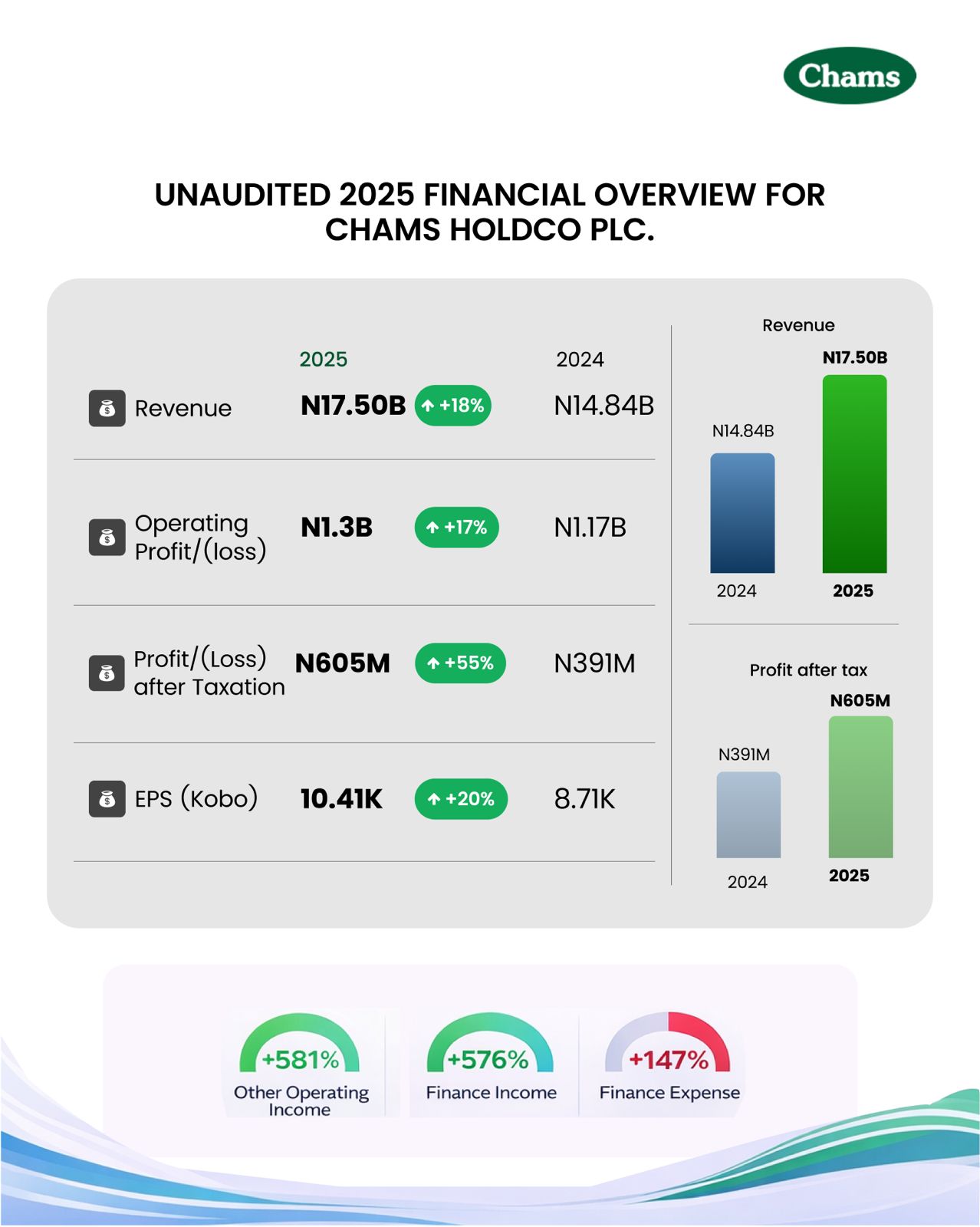

Chams Holding Company Plc delivered robust unaudited results for the year ended Dec. 31, 2025, with revenue climbing 18%to ₦17.5 billion from ₦14.8 billion in 2024. Growth was primarily driven by strong demand in biometrics-related products and SIMs and payment cards. Profit after tax advanced 55% to ₦605.6 million from ₦391.1 million, driving basic and diluted earnings per share higher to 10.41 kobo from 8.71 kobo.

Investor enthusiasm has propelled the stock to new heights. Chams shares reached an all-time high of ₦5.45 earlier this year. The stock has more than doubled overthe past 12 months while year-to-date performance has remained firmly positive.

Strategic Progress and Growth Outlook

Chams marked several strategic wins during the period. The rights issue was oversubscribed by 32.72%, reflecting deep market confidence in the company's governance, strategy, and prospects while injecting fresh capital to fortify the balance sheet and accelerate expansion.

CardCentre has commenced machinery acquisitions to scale up production capacity for card personalization and allied services, directly supporting rising demand. ChamsSwitch continued its strong run, onboarding more banks and users for cross-border payments with Unionpay, which is lifting transaction volumes,enhancing interoperability, and solidifying the group's role in Nigeria's fast-evolving digital payments ecosystem.

Looking forward, Chams remains laser-focused on deepening profitability, strengthening stakeholder confidence, and executing its key strategic priorities. These include building a state-of-the-art card personalization plant, rolling out mobile money and digital payments solutions,expanding the ChamsAccess product across African markets, and deploying next-generation switching technology. These initiatives represent the core objectives funded by the recent capital raise through the oversubscribed rights issue and private placement.